On 5th May 2009, with the world still reeling from the effects of the global financial crisis, a secret gathering of billionaires took place at the elegant but discrete President’s House within the grounds of New York’s Rockefeller University. This event – a dinner arranged by Bill & Melinda Gates and hosted by David Rockefeller – marked the first stage of an ambitious plan devised by Warren Buffett.

Michael Bloomberg, George Soros and Oprah Winfrey were among those invited. Subsequent dinners were held in Manhattan, San Francisco, London, India and China.

The Giving Pledge was announced the following year, with 40 billionaires making a public commitment to give at least half of their wealth to philanthropy during their lifetimes or upon their death.

A decade later and the number of pledgers has increased to over 200, equating to an estimated $500bn in philanthropic capital.

This represents the world’s single largest non-sovereign source of capital. It dwarfs the record annual volume for VC investment in the US, which hit $131bn in 2018.

A number of similar initiatives followed, such as Pledge 1% and Founders Pledge, adding billions more in their own right.

However, the success of the Giving Pledge has been called into question.

WAKING A SLEEPING GIANT

A well-known disconnect persists between the appetite for philanthropy and the amount of money that is actually funding benevolent organisations and initiatives.

The United States, which has built upon the precedent set by the great industrialists-turned-philahtropists Andrew Carnegie and John D. Rockefeller, continues to be a world-leading philanthropic force: it contributes more than two-thirds of the signatures to the Giving Pledge.

However, analysis by the Bridgespan Group shows that the ultra-wealthy families of America are currently donating just 1.2% of their assets per annum – far below average long-term investment returns which are close to 10%.

This means that wealth continues to accumulate: far more is earned in interest, dividends and capital gains than is being donated – despite the clear desire to re-distribute capital to benevolent causes.

Many commentators attribute this disconnect to structural inadequacies in the field of philanthropy. As Kelsey Piper’s Vox article explains, “Giving away a lot of money, if you want to do it effectively, is actually not that easy… The pledge could have had more of an effect if there had been some sophisticated infrastructure for identifying promising giving opportunities that could absorb billions of dollars in funding, and transparently making the case for those giving opportunities to potential funders.”

Furthermore, the findings of a US Trust study revealed that of the high net worth individuals that do make donations every year, “only 40 percent are satisfied with their giving. In general, donors feel either that their money doesn’t have an impact, or that recipients haven’t kept them in the loop regarding milestones and research updates.”

A popular solution is for philanthropy to lean on the principles of private equity (PE). Jeffrey C. Walker, an influential figure in both worlds, outlines a number of ways in which this can be achieved, with the utilisation of more sophisticated tools and infrastructure enabling philanthropic capital to be pooled into professionally-managed funds.

A WOLF IN SHEEP’S CLOTHING?

In the space of a few decades private equity has grown into a multi-trillion dollar industry; it is an incredibly efficient machine for attracting capital, identifying and structuring investments, and generating returns.

Philanthropy needs to quickly acquire such machinery to allow it to manage large volumes of capital effectively and independently.

Philanthropy represents a rich mine in a poor country: it either needs to develop the expertise and infrastructure to retain control over its precious resources so that it can further its own agenda, or risk the foreign powers of PE tapping into its reserves to fuel its own growth. Some element of the latter is inevitable and can already be seen to be taking place.

The burgeoning field of responsible and sustainable investing, which places a greater focus on achieving a positive societal outcome alongside the generation of profit, demonstrates a blurring of the lines between philanthropy and PE: as noted in a McKinsey article, “global sustainable investment now tops $30 trillion—up 68 percent since 2014 and tenfold since 2004.”

Furthermore, the consideration of ESG (environmental, social and corporate governance) factors has quickly become part of mainstream investment appraisal criteria.

However, rather than philanthropy learning from private equity, these trends show the opposite is happening.

An increasing number of funds have learnt to differentiate their proposition to would-be investors by capitalising on rising demand for the generation of returns through more responsible means.

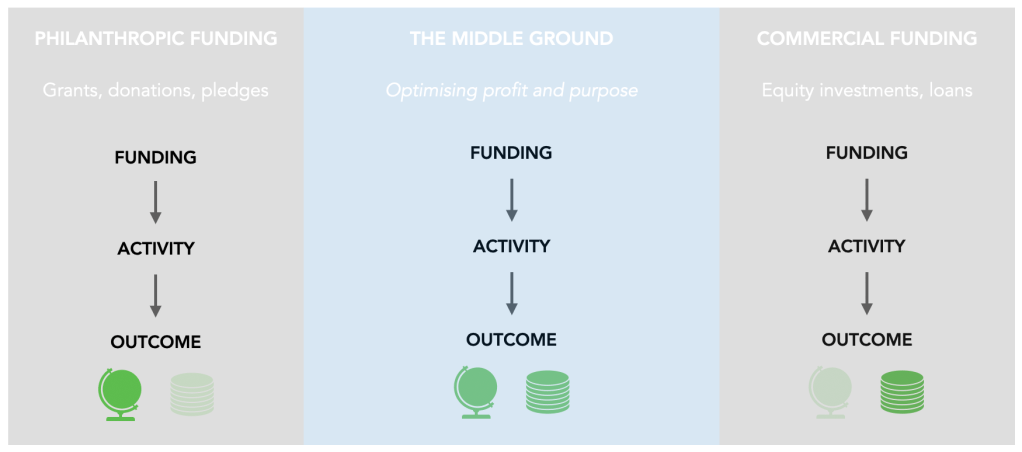

THE FUNDING SPECTRUM

Private equity and philanthropy have traditionally existed as two distinct categories of funding.

PE and venture capital (VC) follow a commercial model, where the focus is on profit. Funding is provided in return for shares in a company; the money is used to grow profits, increasing the value of the business and enabling the investment to be exited at a gain.

Money goes in, more money comes out.

Whereas, philanthropic capital is provided in the form of donations and grants to fund an initiative – usually implemented by a not-for-profit (NFP) organisation – that seeks to achieve positive societal/environmental outcomes.

The focus is on ‘purpose’ rather than profit. Many NFPs are dependent upon donations and grants; once the initiative is completed and the money has been spent, the process must be repeated to achieve further benefit.

Money goes in, societal/environmental benefit comes out.

As summarised by Don Shaffer, CEO of RSF Social Finance, “the dominant model remains a compartmentalized world where venture capitalists aim to make as much money as they can in the shortest possible time and philanthropists give money to donation-dependent nonprofits”.

However, Shaffer continues, “forward-looking funders are taking an approach that crosses conventional boundaries.”

A middle ground is beginning to form between these traditionally distinct categories, which can now be viewed as poles on a spectrum.

Over time, commercial investors have recognised that factoring ESG risks into their investment decisions helps to protect value, particularly in a world of increasing transparency and scrutiny.

This gave rise to a new breed of investors, ranging from those who ‘negatively screen’ for ESG risks, to those who actively work to mitigate them.

Some funds take it a step further, only investing in companies that are directly pursuing environmental and social causes, whilst accepting that the resulting financial returns may be lower than traditional investments.

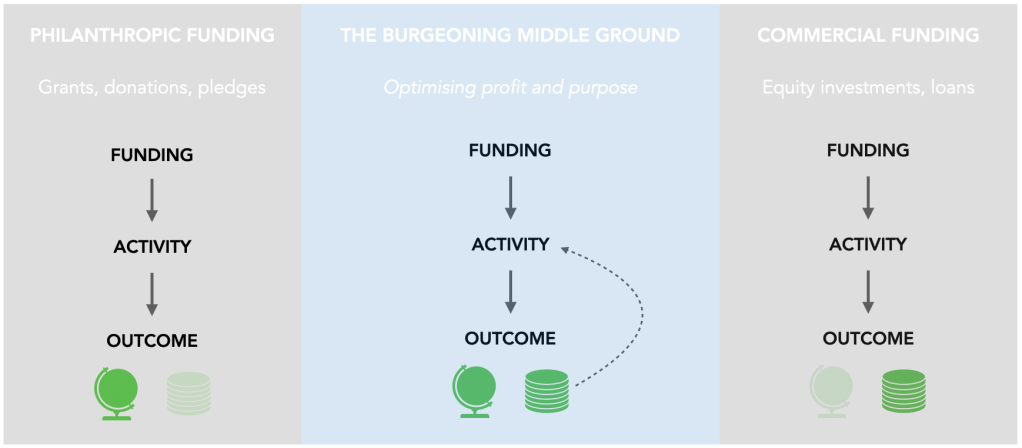

Taking a closer look reveals that much of the middle ground consists of PE funds that have shifted to the left, employing the same underlying commercial investment model whilst incorporating varying degrees of conscience.

The diagram below shows an adjusted view of the Bridges Funding Spectrum:

The ESG boom and the rapidly populous cohort of left-leaning PE funds is the result of the capitalist machine responding to changing demands, which in this case is a growing desire to do better for the planet and society.

Assuming that the capital flooding into this middle ground has flowed from the right side of the spectrum, it is a positive sign that the world of finance is taking a step towards a more responsible future.

But it does not directly address the challenge of mobilising the vast sums of philanthropic capital that will continue to lie dormant or be lured away to the right hand side of the spectrum.

So how can Philanthropy take its own step into the new middle ground and unlock the huge potential of the funds at its disposal?

Capitalism has become more responsible; can philanthropy become more financially impactful?

A STEP TO THE RIGHT

The groundwork has already been laid. Over the last decade, new legislation has paved the way to unlocking philanthropic capital and magnifying its effectiveness.

This followed a gradual realisation that the solutions to the world’s most pressing issues may not lie solely within the public sector and NFPs – but that the dynamism and entrepreneurial spirit of the private sector can also play an important role.

A key development was the creation of a new form of legal entity in the US – the Low-profit Limited Liability Company (L3C). This hybrid structure can be adopted by mission-driven enterprises that have, in the words of Marc J. Lane, a leading figure in this arena, “modest financial prospects, but the possibility of major social impact.”

The L3C form is specifically designed to leverage program-related investments (PRIs) from charitable foundations. These are akin to the commercial funding model in that they can generate financial returns, but that must not be the over-riding goal. If a purely profit-driven commercial funder would make the same investment on the same terms, it is unlikely to qualify as a PRI.

PRIs are an important mechanism for deploying philanthropic capital into the private sector. A foundation must distribute 5% of its assets every year in order to maintain its tax-exempt status. The majority of this distribution is in the traditional form of philanthropy outlined above: donations and grants. But PRIs can also be counted towards the 5%, provided that the primary objective of the investment (and its recipient) is to further the underlying purpose of the foundation, and that the generation of profit is not a significant goal.

The Gates Foundation – an extremely influential force in the new age of philanthropy – launched a dedicated PRI fund in 2009, now called the Strategic Investment Fund. However, foundations have largely shied away from PRIs due to the grey area left between purpose and profit and the risk that an IRS audit would subsequently view an investment as insufficiently purpose-driven and overrule the eligibility of the PRI – with the potential to cause significant tax complications for the foundation.

L3Cs avoid this ambiguity. In an interview with Forbes, Lane explains that “by statute, the L3C is obligated to be mission-driven and that mission is superior to profits.”

Several US states have passed legislation to authorise L3Cs, providing clarity and assurance to foundations that funding such companies will be classed as a PRI.

Whilst the L3C is the most direct link, additional forms of legal entity (such as Benefit Corporations) have proliferated, helping to channel philanthropic capital into worthy private sector recipients.

Companies that pursue a benevolent purpose and have the potential to generate profit alongside a positive environmental or social impact (herein referred to as a ‘purpose company’) can be an extremely effective means for unlocking the potential of philanthropy.

LINEAR VS CIRCULAR PHILANTHROPY

A big advantage of using philanthropic capital to fund a purpose company is that the capital can be recycled.

Instead of the linear ‘money in, benefit out’ model of traditional grants and donations, a purpose-driven company can generate profit alongside social/environmental impact.

Linking purpose with profit is an incredibly efficient way of propagating benevolent causes. Not only does the purpose company re-invest its profits to generate an ever increasing impact, but it also shows the market that such activities can be profitable, and other private sector companies will follow suit.

Furthermore, philanthropic investments into purpose companies have the potential to be exited at a gain in the future, allowing the capital to be returned to the fund or foundation and redeployed.

PRIs can therefore unlock a huge amount of impact per unit of philanthropic capital.

As explained by British philanthropist Sir Harvey McGrath, who allocated an initial £1.5m into a Donor Advised Fund (a vehicle from which such philanthropic investments can be made): “the funds have been recycled many times, so that my initial investment has enabled a total commitment of £6.6m in more than 400 deals.”

“Philanthropy’s shift to seeking both social good and financial return could be our best bet when it comes to filling the social-innovation funding gap”, states Christian Braemer, CEO of Benefunder, in a Stanford Social Innovation Review article.

Such investments are not only able to plug this funding gap, known as the ‘valley of death’ – when early stage companies do not yet have the commercial traction to secure traditional sources of funding, but require capital to reach that point – but they also have the added benefit of attracting subsequent VC or PE investment.

INVESTING VS GIVING

The valley of death must be navigated by all innovative businesses in their nascency, but for those with the noble objective of shaping a company around a benevolent purpose there is the added challenge of balancing that purpose with financial viability.

A relentless pursuit of profit too early may undermine the purity and effectiveness of a societal or environmental purpose.

People, planet and profit do not need to be prioritised over one another; sustainable and socially beneficial business models can also be better for the bottom line. But obtaining that equilibrium is a precarious balancing act during the infancy of a company.

To safeguard the benevolence of a purpose company, it may be best to remove financial metrics from the equation – at least initially – and for philanthropy to build out from its heartland of grants and donations.

There is a fundamental difference between investing and giving. Perhaps some philanthropic investments risk straying too far to the right hand side of the funding spectrum – and have leapfrogged the opportunity gap identified on the diagram above. A more natural first step to the right would be to retain the traditional mechanics of philanthropy and provide funding to early stage purpose companies in the form of grants.

Not being treated as a traditional equity investment provides more room for the purpose company to focus on delivering impact. Indeed, a criticism of L3Cs is the conflict that can arise between different stakeholders once traditional commerical funders become involved, and how to balance purpose with fiduciary duties.

THE ELEPHANT IN THE ROOM

As soon as financial returns are brought into play, priorities can swiftly change. The ideal scenario would be for a purpose company to raise sufficient grant funding to see it through its formative stages – to the point at which it has developed an organisational structure, system of governance and a culture focussed on delivering its purpose effectively, whilst having demonstrated an ability to monetise it.

This would be the foundation upon which to foster the commercial performance of the company.

The elephant in the room is the scenario where the purpose company does become profitable as a result of its benevolent trading activity, which is of course the desired outcome. Should the philanthropic entity that provided early stage grant funding be entitled to some form of return?

The potential for a financial upside should not be excluded, but must be considered and structured carefully.

A number of mechanisms for achieving this have already been conceived and implemented.

They are summarised in the paper ‘Full spectrum finance: how philanthropy discovers impact beyond donation and investments’.

Referring to the fallacy that “business models either return at -100%, and thus require donations or subsidies, or return well above inflation rate, and thus attract loans or equity”, the authors state that, despite the vast majority of capital channeled to the two ends of the spectrum, “the most interesting ideas live between these extremes, and clash with the expectations of traditional donors and investors alike.”

The authors recommend that philanthropists “deploy a broad range of financial instruments covering the full spectrum of financial returns from -100% all the way up to positive returns.”

CONVERTIBLE GRANTS

The most interesting and potentially impactful of these instruments is the convertible grant.

Here, the purpose company receives early stage philanthropic funding in the form of a traditional grant, thus avoiding undue pressure on financial metrics during its infancy – but with the potential for the grant to subsequently be converted into equity, thus enabling the philanthropic fund to realise a return and recycle the capital.

The success of convertible grants will hinge upon carefully defined triggers for conversion, and how the relationship with the company is managed once the donor transitions to an investor.

Conversion triggers will of course need to be specific to each case, but in general they would be best linked to external events rather than performance metrics of the company itself. This helps avoid a conflict of interest and undue pressure to hit arbitrary targets.

Such events could include a subsequent VC/PE investment, or a sale/change of control – both of which demonstrate the comercial success of the company through an external point of validation.

The mechanics of conversion could be similar to those of VC convertible loan notes, with the discount (and/or valuation cap) increasing in line with metrics that indicate the commercial progression of the business, or the nature of transaction (from minority stake investments through to buy-outs and IPOs).

There could also be a backstop date for conversion, after a sufficient period of time for the commercial viability of the purpose company to have been determined: if the company is still operating after five years for example, it is likely that it is a commercial success.

If financial targets are set, they should be on a sliding scale basis rather than all-or-nothing, to avoid the risk of dysfunctional behaviour concerning the achievement of arbitrary metrics.

GREAT MINDS, FOR THE GREATER GOOD

Whilst conversion mechanics are objectively complex, it is the intangible dynamics of relationship management between the philanthropic entity and the purpose company that will likely be the most challenging to get right.

Conversion from grant to equity should mark the handover to a different support team, from one with a charitable/purpose focus to one with a commercial/profit focus. A different type of professional will be best suited to one or other of these stages of the relationship.

Philanthropic funds of the future will likely split their portfolio teams, with a handover to investment professionals once shares are obtained; by this time the culture and governance of the business has been established, and the benevolent trading activity has demonstrated commercial viability. More steer from a financial perspective would at this point not only benefit the company, but also the fund (increasing the likelihood and quantum of a return that can then be recycled) and the underlying philanthropic cause (by demonstrating to the market that such activities can be financially lucrative).

However, there should still be a level of continuity and the purpose element of the equation must not be neglected – some oversight from the charitable arm should remain.

Whilst the focus throughout this piece has been on the perspective of the philanthropist, it is worth considering that of those who will be the founders of purpose companies. In doing so, the argument for convertible grants becomes even stronger.

The availability of non-dilutive funding capable of bridging the valley of death is an extremely attractive proposition to a would-be founder of a purpose company. Not only can they avoid ceding control of their business, but they will have a greater share of the upside – the grant only converts to equity when commercial success is proven, and it coverts to a lower amount of equity than a traditional investor would demand (in order to be classed as a PRI).

Whilst purpose companies may not have as lofty valuation prospects as a purely profit-driven enterprise, the availability of early stage funding that allows the founder to keep control and a larger share of future exit proceeds should help to attract and incentivise more scientists, engineers and entrepreneurs.

Convertible grants can therefore unlock the full potential of human capital and philanthropic capital – ensuring that the world’s best minds are working on solutions to the world’s greatest challenges.